Rolling over your 401(k) is like sending your grandma flowers: we all think we should probably do it, but most never get around to it. It takes a couple of hours and might be the most valuable time you spend in your life (This is true for the grandma flowers too). Here are the reasons why. #4 saves you almost a million bucks, so don’t skip out early!

1. Simplicity

In 2016 the average employee tenure was 4.2 years. In a 40 year career that would be more than nine different jobs. If each of those jobs offered a 401(k) you could have nine accounts floating out there. Do you know where each and every one is? Have all the login information? Know how much is in there? Are they invested in the right stuff? Losing track of one of them could cost you tens or hundreds of thousands of dollars. Rolling over to a central, personal IRA keeps everything where you know it is.

2. Cut Ties With Former Employers

401(k)s are employer sponsored retirement accounts. Once you leave a job, that employer generally doesn’t give a shit about you. But when you want to go back and get your money out, you might need to work with them again. Lost your account info? Talk to your old boss or HR department. Can’t remember what bank it’s with? Hope your old company is still taking your calls. Your old company has since been acquired or gone out of business? Now what? Rolling over to your own personal IRA cuts your old company completely out of your life!

3. Unlimited Investment Options

When you sign up for a 401(k) you are given a list of investment options. Those options are decided by your employer. Often they suck. It’s still very worth it to invest for the tax benefits, but once you leave do a rollover to your own personal IRA and invest in whatever you want! (Hint: Buy and hold index funds)

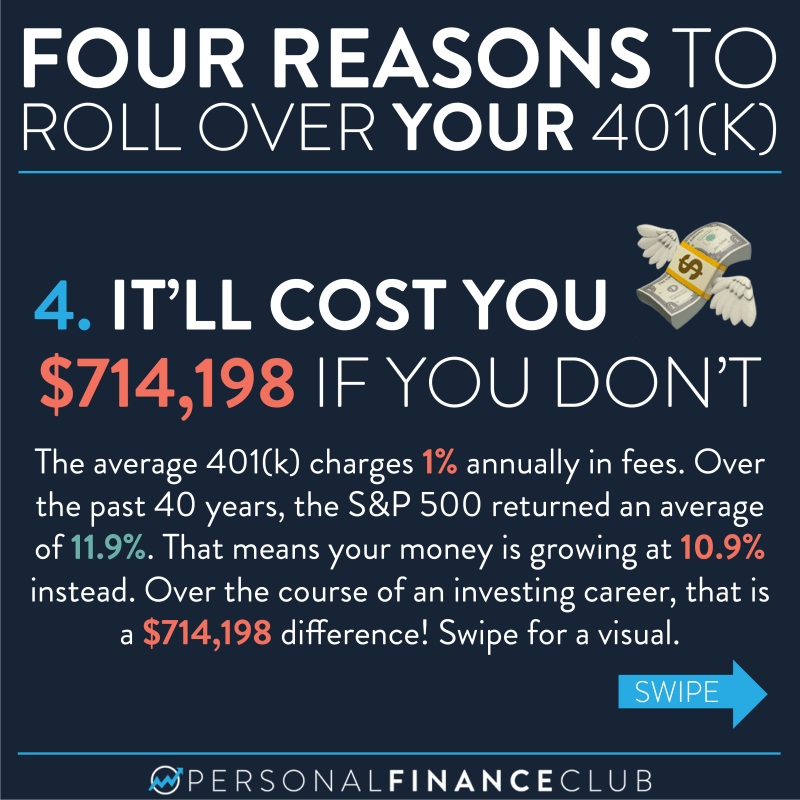

4. It will cost you $714,198 if you don’t

Stay with me here because we’re gonna do some math.

- The average 401(k) charges 1% annually in fees. (It’s even worse if your 401(k) was with a small business which generally have higher fees)

- A personal Rollover IRA can have fees as low as 0%. (If you invest in Fidelity’s 0% index funds, or very close to 0% with most brokerages’ index funds)

- An S&P 500 index fund has gained 11.9% per year on average over the last 40 years based on this calculator (with dividends reinvested).

That means instead of your money growing at 11.9% it’s growing at 10.9%. That doesn’t sound terrible, but remember the power of compound growth! Let’s say you started investing $250/month at age 25. At 11.9% your money would grow to $2.8M when you are 65 as opposed to $2.09M if you were earning 10.9%. That means you’re kissing $714,198 away if you pay the 1% fees. Here’s a visual of this example:

That’s still kind of a lot of numbers so here’s a picture of what that $714K could have bought you:

It’s brand new, 43 feet long, cruising speed of 35 knots and you just pissed it away by not rolling over your 401(k). (It’s actually listed on yachtworld.com for $691,985 so you’ll have money left over to throw a massive party for your friends who don’t have yachts because they didn’t roll over their 401(k)s).

And there is one reason why you may NOT want to rollover your old 401k! That’s if you’re likely to be doing backdoor Roth IRAs in the future. If you are, then it’s made simpler and cheaper if you don’t have any money in a traditional or rollover IRA (this avoids the “pro-rata” rule). In this case you could leave the 401k where it is, or roll it over to your new employer’s 401k if you have one!

So please, roll over your 401(k) and send Grandma some flowers!