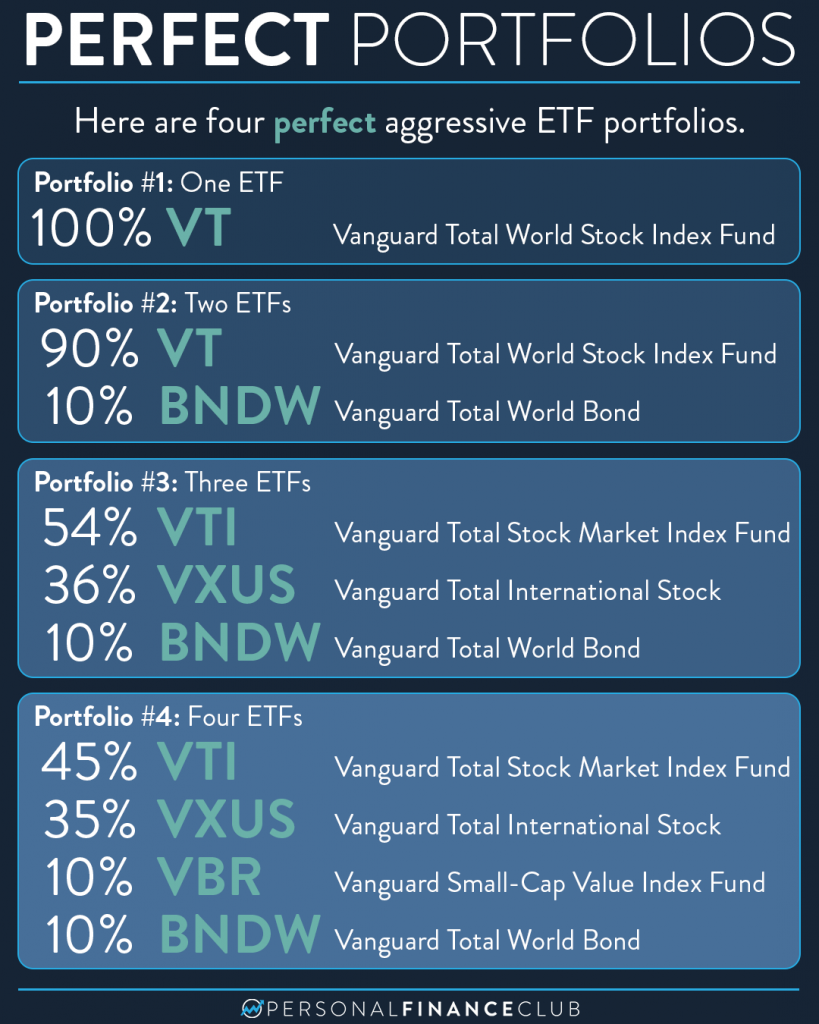

If you sat down with me and showed me your investment portfolio and you showed me any one of these four portfolios I would say “Congratulations. That’s a fantastic portfolio. A+. No notes”. One of the most challenging part of investing is having the confidence to keep it this simple and stay the course. But those who do will be greatly rewarded.

How can it be that all four of these portfolios are “perfect” even though they’re different?! Well, first, they have way more in common than they have different. They all own virtually all of the companies of the world, in proportion to the size of the companies. They also all have extremely low costs in the convenient package of an ETF. Additionally, there is no single “perfect” portfolio. The best we can do is choose one of many perfect portfolios and stick with it. I used Vanguard ETFs in this example, but you could use Schwab or iShares ETFs (these days in the US all ETFs trade free on virtually all brokerages) or you could use the mutual fund version of index funds from Vanguard, Fidelity, or Schwab.

Ok, what about the differences? Portfolio one and two are obviously different because one contains bonds and one doesn’t. That’s true, but both contain at least 90% stocks! If you’re in the “aggressive” portion of your wealth building journey, choosing between 90% stocks and 100% stocks won’t make much difference. Picking one, sticking with it, and putting more money in WILL make the difference.

Isn’t portfolio 4 more diversified than portfolio 2? Nope! There’s no stock or bond that’s in portfolio 4 that’s not in 2. Buying more ETFs doesn’t make make you diversified, if you already own broadly diverse ETFs.

Then what’s VBR? There’s some evidence that over long periods of time small cap value stocks out perform the total market (although you may need to accept more volatility to achieve that). If you want to “tilt” your portfolio toward small cap value, I still give you an A+. But you don’t have to.

As always, reminding you to build wealth by following the two PFC rules: 1.) Live below your means and 2.) Invest early and often.

-Jeremy