September Sale!

September Sale!

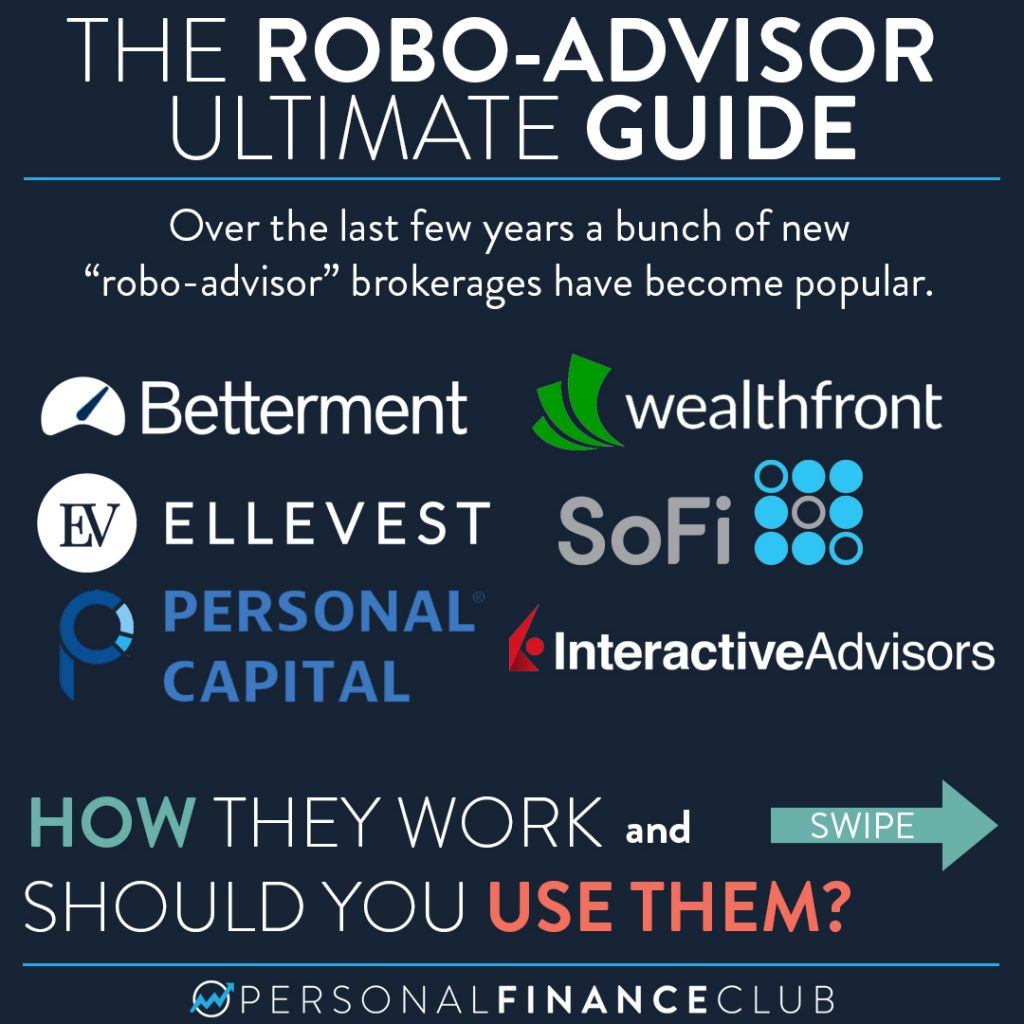

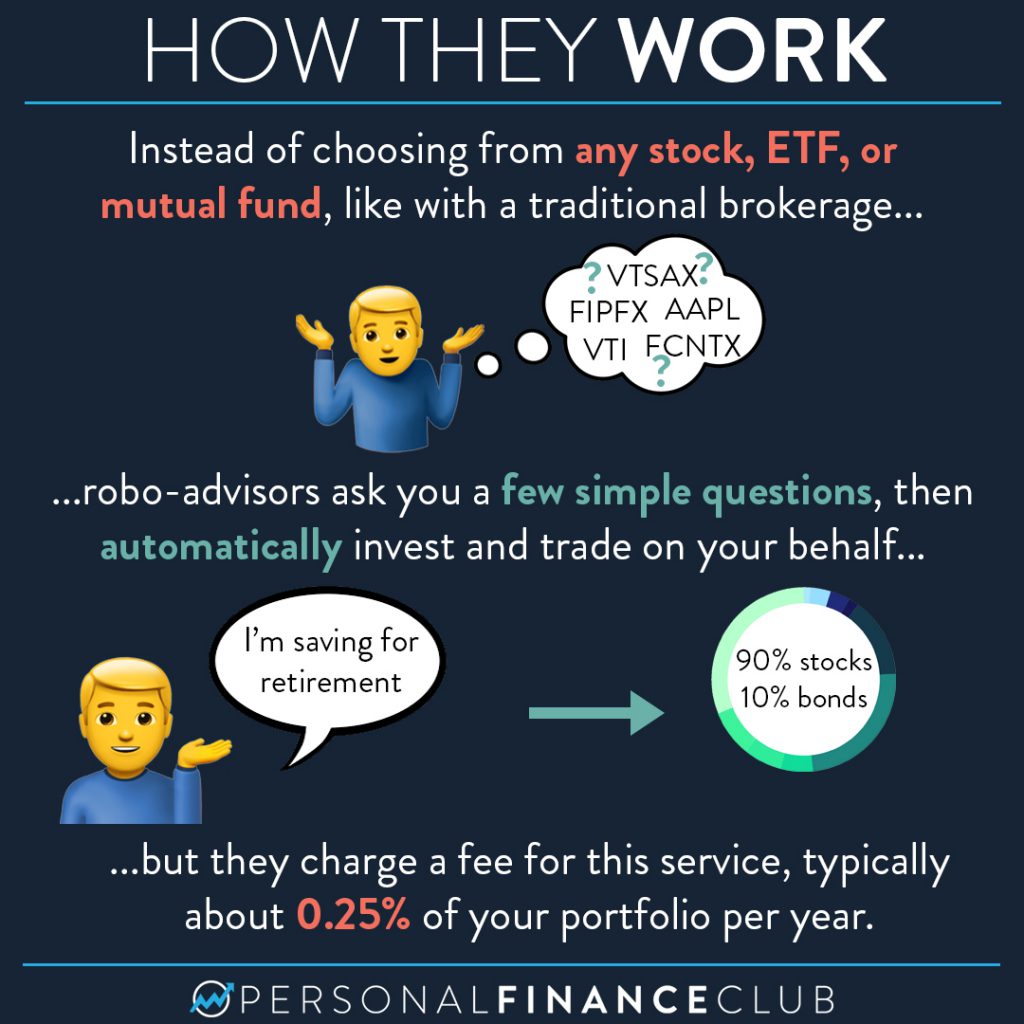

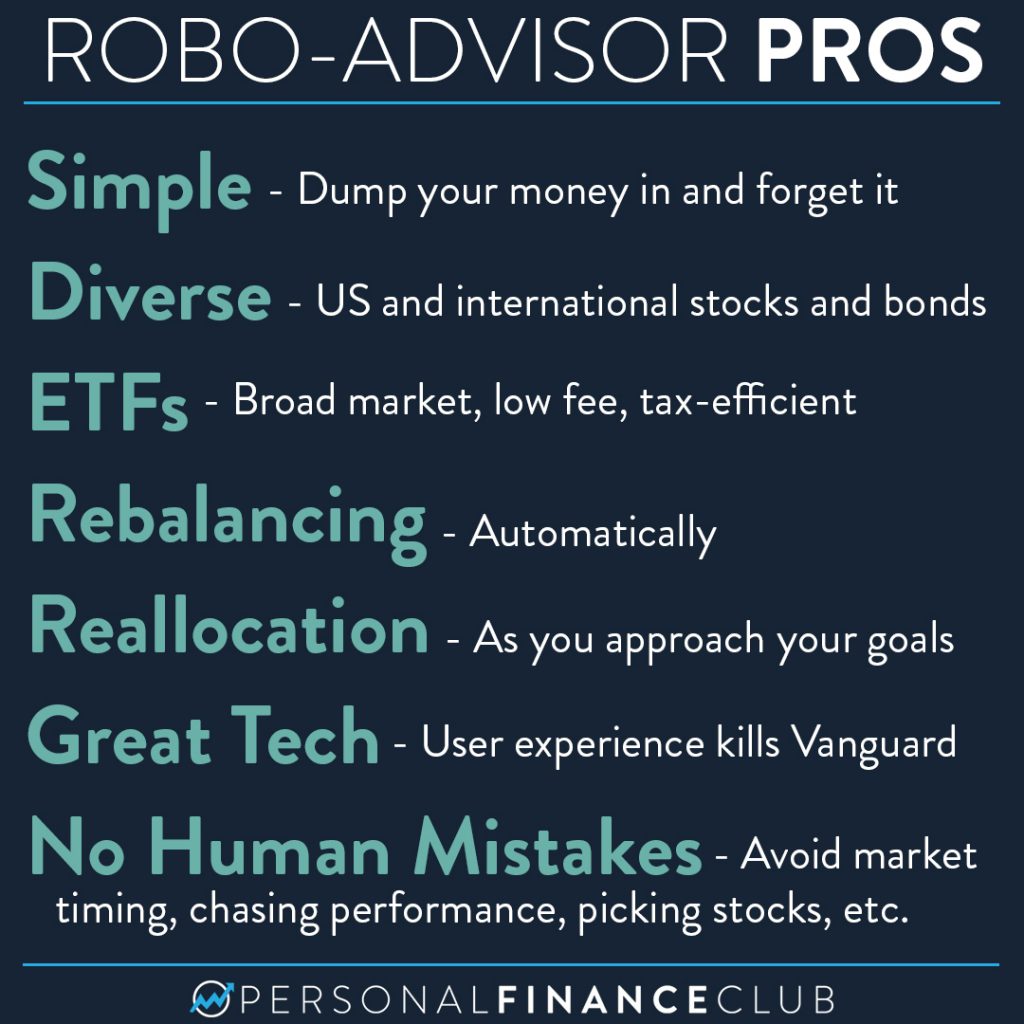

I don’t hate robo-advisors. I could have even seen myself starting a robo-advisor company if the timing was right! They’re really cool. As this post shows, there’s tons of benefits to using them. They make investing easy. Opening a traditional brokerage account can be intimidating (I have some step by step guides on how to get started down my page). I really like that they’re lowering the bar to get started investing, and making it an easier experience, just like any modern app in the app store.

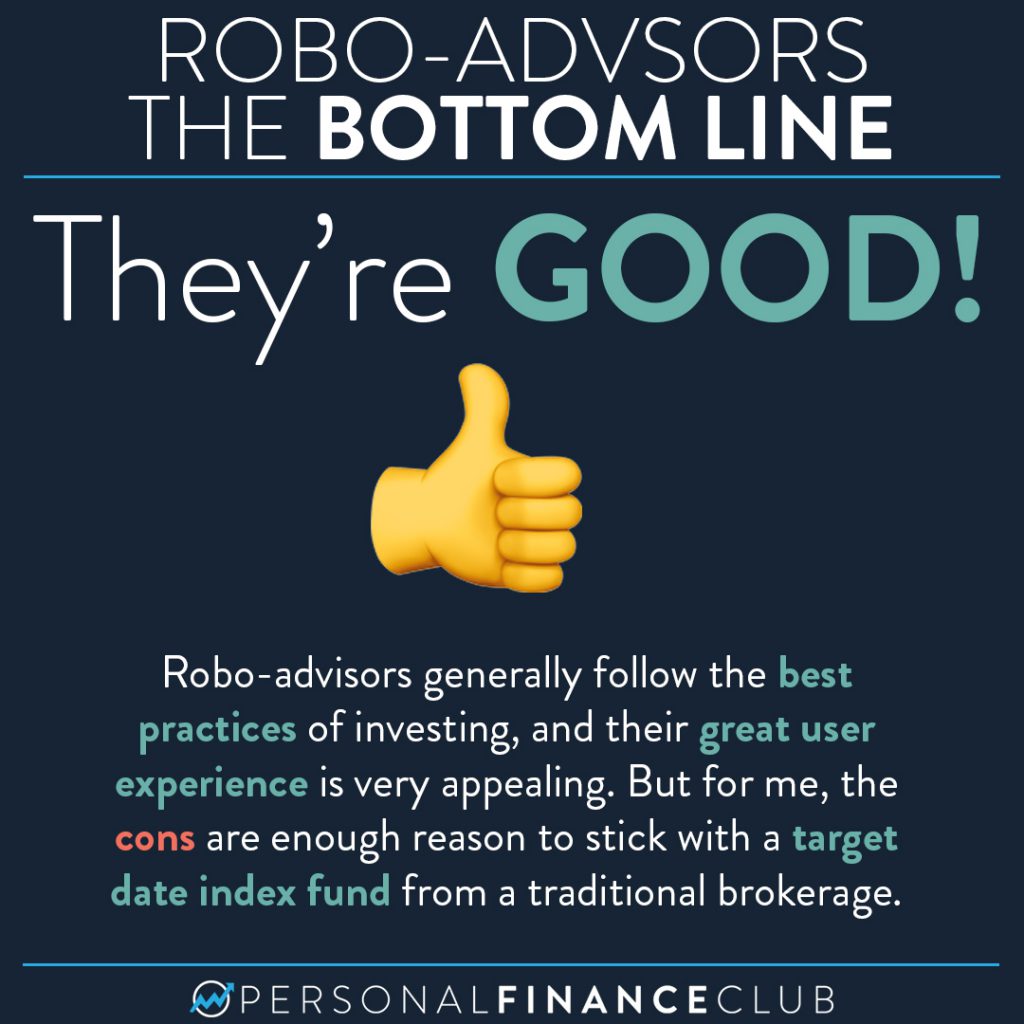

If you like your robo-advisor, stick with it. If you’re more likely to contribute more money because you think it’s fun, boom. Definitely stick with it. If you love the user experience and just can’t deal with Vanguard’s website anymore. Hey, that’s legit. Stick with it. If you’re afraid of opening a traditional brokerage account, but you would invest with a robo-advisor, sweet! That’s a great way to get started.

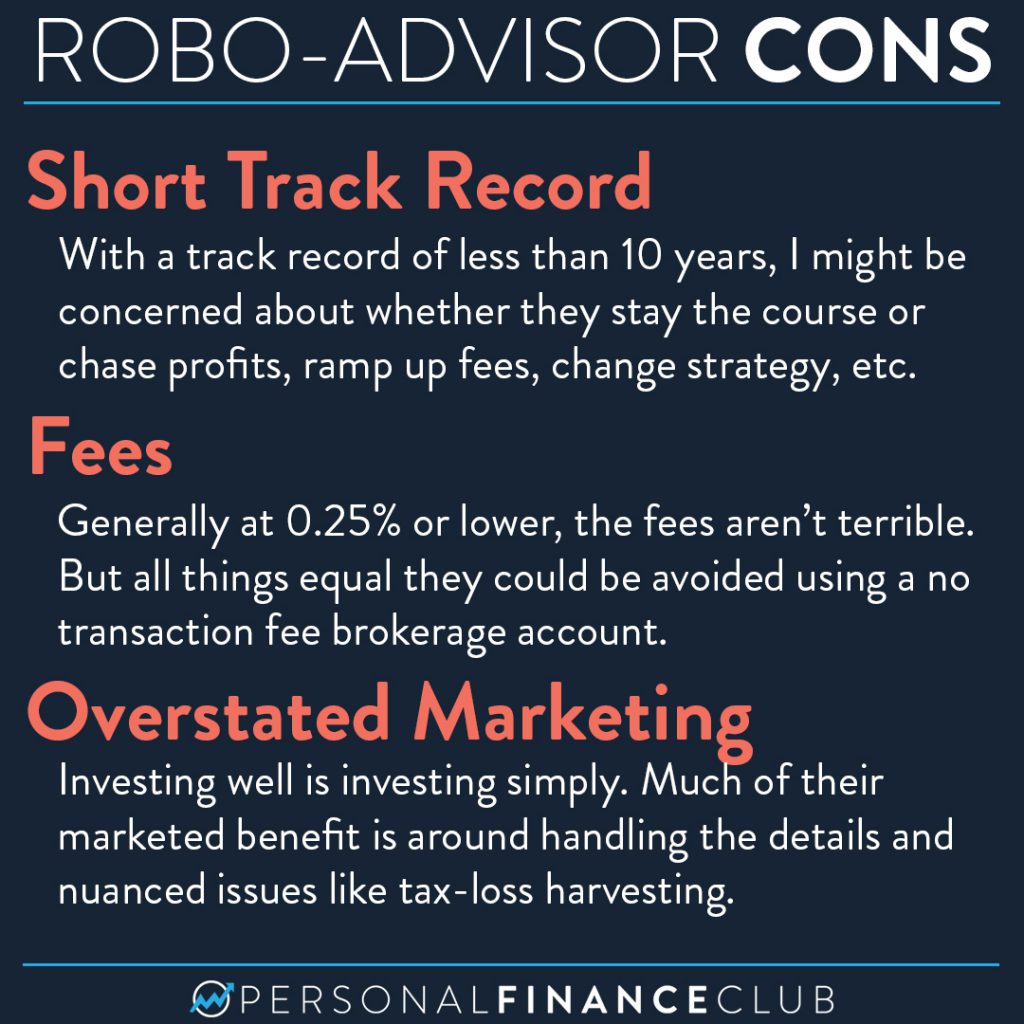

For me, the small additional fee (0.25% on my $2.5M invested is about $6,250/year. I’d rather reinvest that) and the short track record of how these companies behave is enough to keep me with a traditional brokerage (Most of my money is with Fidelity, and I have a small Vanguard account).

That’s my nuanced answer on robo-advisors! They definitely qualify for rule #2 of PFC.

As always, reminding you to build wealth by following the two PFC rules: 1.) Live below your means and 2.) Invest early and often.

– Jeremy

via Instagram