Don’t worry about buying the exact right target date fund. There are a couple key considerations, but outside of that it doesn’t really matter which one you buy.

First make sure that you are using a low fee target date index fund. And, you should always use one that is “transaction free” based on what brokerage you’re with. So, if you use Fidelity, buy a Fidelity target date index fund. Otherwise you have to pay a $75 transaction fee. Which is absolutely ridiculous.

As a warning, not all target date funds are INDEX funds. Some are actively managed, meaning you pay a much higher fee for someone to try and outperform the index. However, this is NOT worth paying because they very rarely actually outperform. And they never do it consistently.

To take a step back, what are target date funds? Each target date fund holds several funds that invest in things like the US stock market, international stocks, and bonds. They are named after a target retirement year. As time goes on they move from a heavy stock allocation to maximize growth while you’re young, to a heavy bond allocation to provide income and capital preservation in retirement.

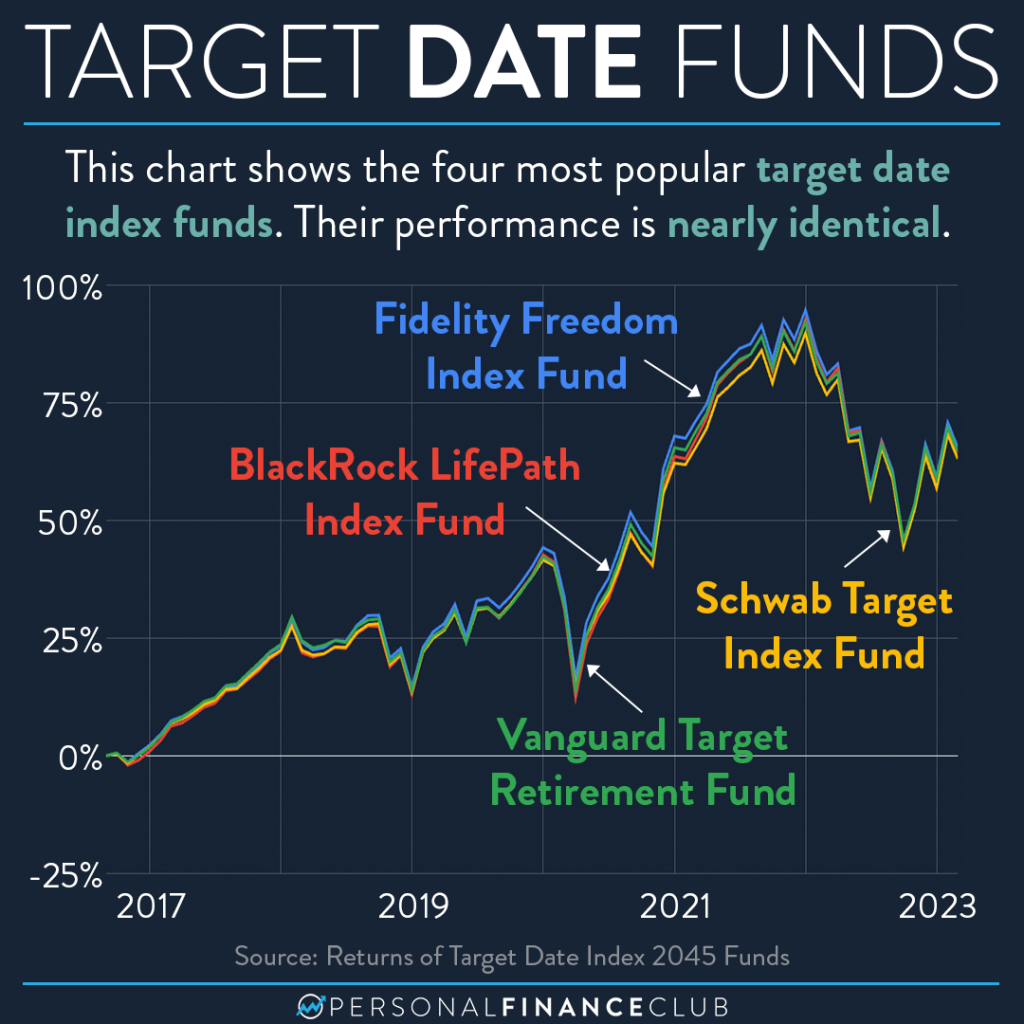

The graph goes back to fall of 2016 when Schwab launched their index target date funds. If you take the other three funds back ten years, it’s very much the same story. All the lines are on top of each other. Also, we used the 2045 fund just as an example, but the performance is nearly identical when comparing other years with each other.

As always, reminding you to build wealth by following the two PFC rules: 1.) Live below your means and 2.) Invest early and often.

-Vivi & Shane