July Sale!

July Sale!

I often get asked “what actual funds do you invest in”? I’m always hesitant to answer without giving context, because what I’m currently invested in is mostly a relic of past decisions, but it’s slightly different than what I would choose going forward.

But given the context of the post, I’ll answer the question here. Most of my money is in the following funds:

• ITOT (Total US Stock ETF)

• IJR (Small Cap Stock ETF)

• IEFA (Non-US Stock ETF)

• IEMG (Emerging Markets Stock ETF)

• BCHYX (California municipal bond fund)

• FSRNX (Real Estate Index Fund)

Notably, I dropped IFGL (international real estate), DBC (commodities), and TIP (treasury inflation protected bonds). I still maintain the six above for two main reasons. One, I believe in “staying the course”. If I swapped entire portfolios every time I had a slightly different idea about investing that would introduce a lot of churn and complexity that would hurt me and may encourage chasing past performance. And two, taxes. I have a lot of unrealized gains in the funds above, so all things equal I’d rather pay the taxes later than today.

It’s a good portfolio, but it’s not what I do going forward. Going forward, I keep things simpler. When I put new money into my Vanguard account, it goes into this portfolio:

• VFIFX – 100% (Vanguard’s 2050 Target Date Index Fund).

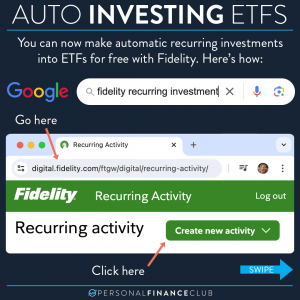

When I put new money into my Fidelity HSA, it goes into this portfolio:

• FIPFX – 100% (Fidelity’s 2050 Target Date Index Fund).

When I put new money into my Vanguard 401k account it goes into this portfolio:

• VFIFX – 90% (Vanguard’s 2050 Target Date Index Fund).

• VSIAX – 10% (Vanguard’s Small-Cap Value Index Fund).

I added that small-cap value fund because there’s SOME evidence out there that it may help contribute to slightly higher returns in the very long time frame (like 40+ years). But if I’m being honest, I’m probably a little guilty of introducing complexity and chasing past performance. Simplicity usually wins out.

As always, reminding you to build wealth by following the two PFC rules: 1.) Live below your means and 2.) Invest early and often.

-Jeremy