July Sale!

July Sale!

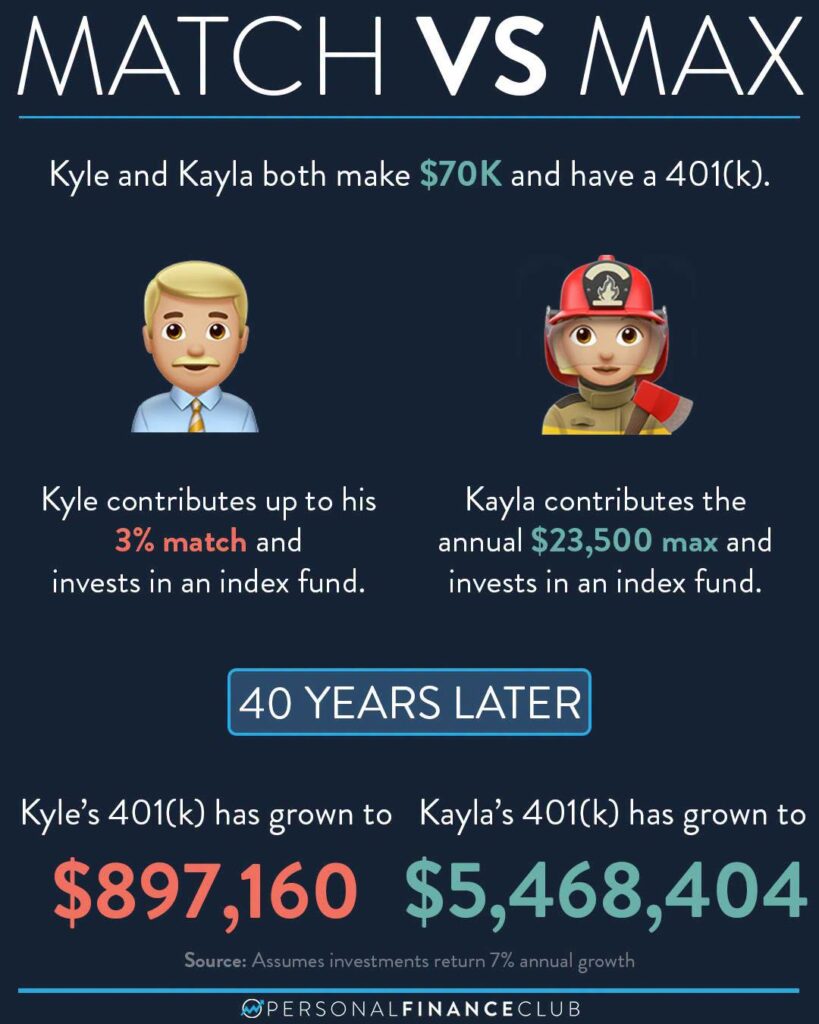

If you get a job that offers a 401k (or 403b, 457, or TSP) you’ll have an opportunity to sign up. During that sign up process you’ll be presented with a choice. What percent of your salary do you want to contribute into this account?

Kyle and Kayla made different choices. Kyle knew that his company offered a 3% match, so in order to take advantage of that, he contributed his own 3%, for a total of 6% of his annual salary getting deposited to his 401k. On a 70K salary, that’s $4,200/year going into his 401k. That amount getting a 7% rate of return over 40 years turns into $897,160. Not bad!

But on that fateful day when Kayla saw the little “How much do you want to contribute” slider on her 401k website, she decided to go nuts. She dragged it all the way to the right. That redirected the IRS max of $23,500 of her salary into her 401k. Her company still gave her the 3% match, which by law doesn’t count against the $23,500. That meant Kayla was contributing a total of $25,600 per year to her 401k. Her investment, getting the same 7% return over 40 years turned into over $5 MILLION BUCKS.

During their working years, Kayla brought home a little less of her salary. Kyle brought home $67,900 (before tax) compared to Kayla’s $46,500. Does Kyle have way more fun with his bigger take home pay? Nah, Kyle is kinda lame and spends all his money on mobile game in-app purchases. Kayla is a badass and spends her time mountain biking, surfing and drinking two-buck-chuck with her friends. Oh, and she retired a multi-millionaire. Or maybe she retired 15 years early with more money than Kyle had at full retirement age. Kayla’s got OPTIONS.

So when you’re deciding how aggressively to invest, think if you want to be more like Kyle or Kayla. (And for the love of god, please don’t be like Kevin who didn’t contribute at all!)

As always, reminding you to build wealth by following the two PFC rules: 1.) Live below your means and 2.) Invest early and often.

-Jeremy & Jenn