I get asked this question a lot. “Should I buy indexed universal life insurance”? It sounds pretty good. After all it has the word INDEX built right into it, right?! But my answer is no. Here’s why:

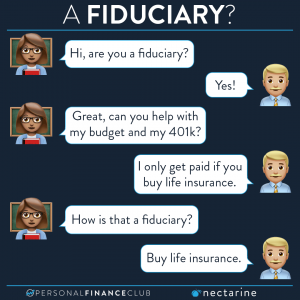

• High commissions. Without fail, whenever I am asked about this it’s because a commissioned salesperson (perhaps even calling himself a financial advisor) is recommending it. Whenever a person earns commission from the sale of a thing he recommends, it’s a good idea to consider his incentives.

• High premiums. The premiums on these are generally several hundred dollars per month. If you throw that into a Roth IRA for a few decades it will likely turn into about a million bucks. I’d rather have that than an insurance policy with a (much smaller) cash value.

• So f*&king complicated. I’m a pretty smart dude. And I’m pretty good at understanding complex topics and breaking them down simply. But these whole life insurance policies are insanely complicated. The rules are dizzying. Trying to understand how much money you get is virtually impossible. And guess who benefits from this insane web of rules set up by the insurance company. Not you. As they say, “Complexity does not favor the investor”. This game is not set up to make you win.

• Nonsense tax benefit. Insurance salespeople LOVE to tout the amazing deferred tax benefit of whole life insurance. But here’s the thing: That tax benefit sucks. It’s way worse than either a traditional or roth IRA or 401K. And it’s about equivalent to the tax efficiency of holding an index fund in a taxable account. But with WAY HIGHER FEES and LOWER RETURNS and your money LOCKED AWAY inside of an insurance policy. It’s not worth it.

Some people are going to light me up in the comments for this. When I peek at their profile I usually see that they earn commission from selling these policies. As they say, “It is difficult to get a man to understand something when his salary depends upon his not understanding it.”

As always, reminding you to build wealth by following the two PFC rules: 1.) Live below your means and 2.) Invest early and often.

– Jeremy

via Instagram