I’m 39 years old, I became a millionaire at 34, and I retired at 36. I’ve been living in the same one bedroom apartment for the last five and a half years. It’s a converted garage owned by my friends who live in the attached house. My rent is $1,350/month, which is pretty good for San Diego. Every month I live here and don’t buy my own place I am becoming more wealth than if I bought a home.

The title of this article will be true for about another month, at which point I’m moving into the two bedroom condo I recently purchased. During this time of housing transition, I wanted to discuss the “rent vs buy” question that plagues so many. Spoiler alert: I think that’s the wrong question to be asking. The more important factor is minimizing spending on your primary residence whether you rent or buy.

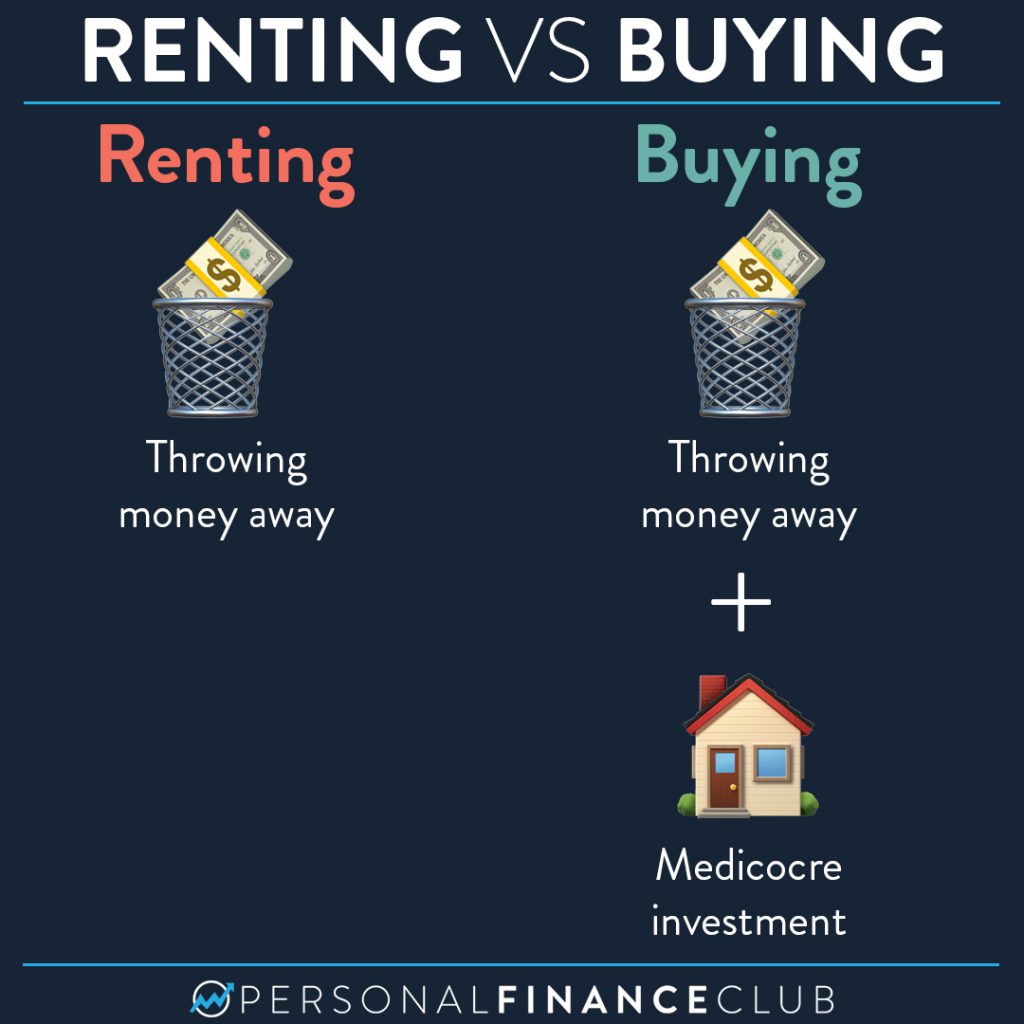

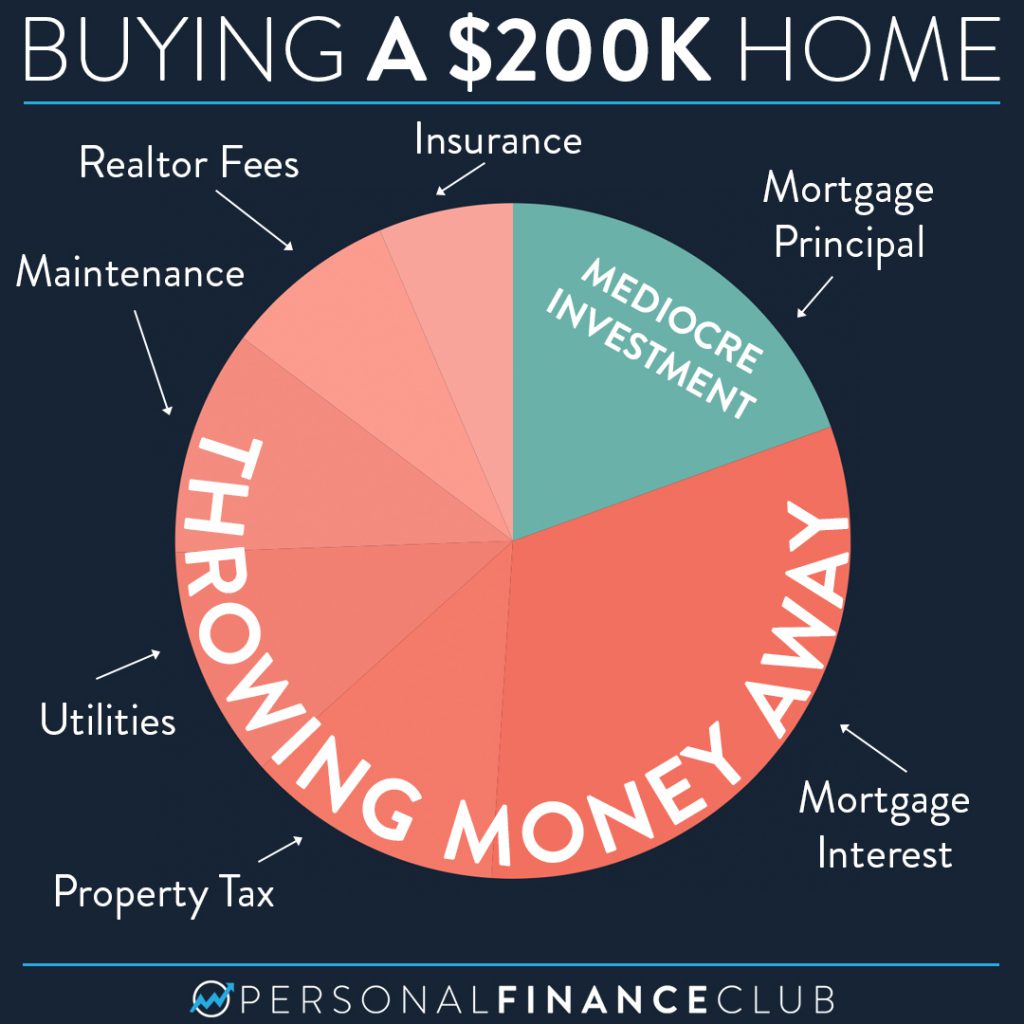

Homeowners love to look down their noses at renters and inform them that renting is throwing money away. The logic is pretty straight forward. Why burn all that money on rent, benefiting only your landlord, when you could be paying down a mortgage and have all of it go into your own pocket?! But here’s the problem. When you own, MOST of your monthly expense is also being burned on totally sunk costs. When you buy, your housing expense includes mortgage interest, property tax, property maintenance, homeowner’s insurance, utilities, realtor fees, closing costs, possibly HOA fees, and finally some money goes towards mortgage principal. According to the National Association of Home Builders, homeowners stay in one home for an average of 13 years. Based on buying a $200,000 home, the current US median price, here’s a look at an average month of homeownership expenses halfway through those 13 years based on a 30 year mortgage.

Buying a $200,000 house 6.5 years into 30 year mortgage @ 4%

| Mortgage Principle | $301 |

| Mortgage Interest | $486 |

| Property Tax | $190 |

| Utilities | $172 |

| Maintenance | $167 |

| Realtor Fees | $128 |

| Insurance | $99 |

| Total | $1,543 |

Of the $1,543 spent on housing in this example month, only $301 went to the principal paydown of the mortgage. All those other expenses are “throwing money away” in the exact same way that rent is.

And that $301 going towards rent historically hasn’t been a magnificent investment. Over the last 32 years the US National Home Price Index has grown at a rate of about 3.8% annually. Over that same period, the S&P 500 has grown at a rate of about 10.0%. That means a $100,000 house bought in 1987 would be worth about $332,800 today. Meanwhile a $100,000 investment in an S&P 500 index fund in 1987 is now worth about $2,292,000.

The entrance fee of burning 80% of your monthly payment grants you the ability to put the 20% in an asset returning 3.8%. That is not math for great investment success.

Rent vs Buy is the Wrong Question

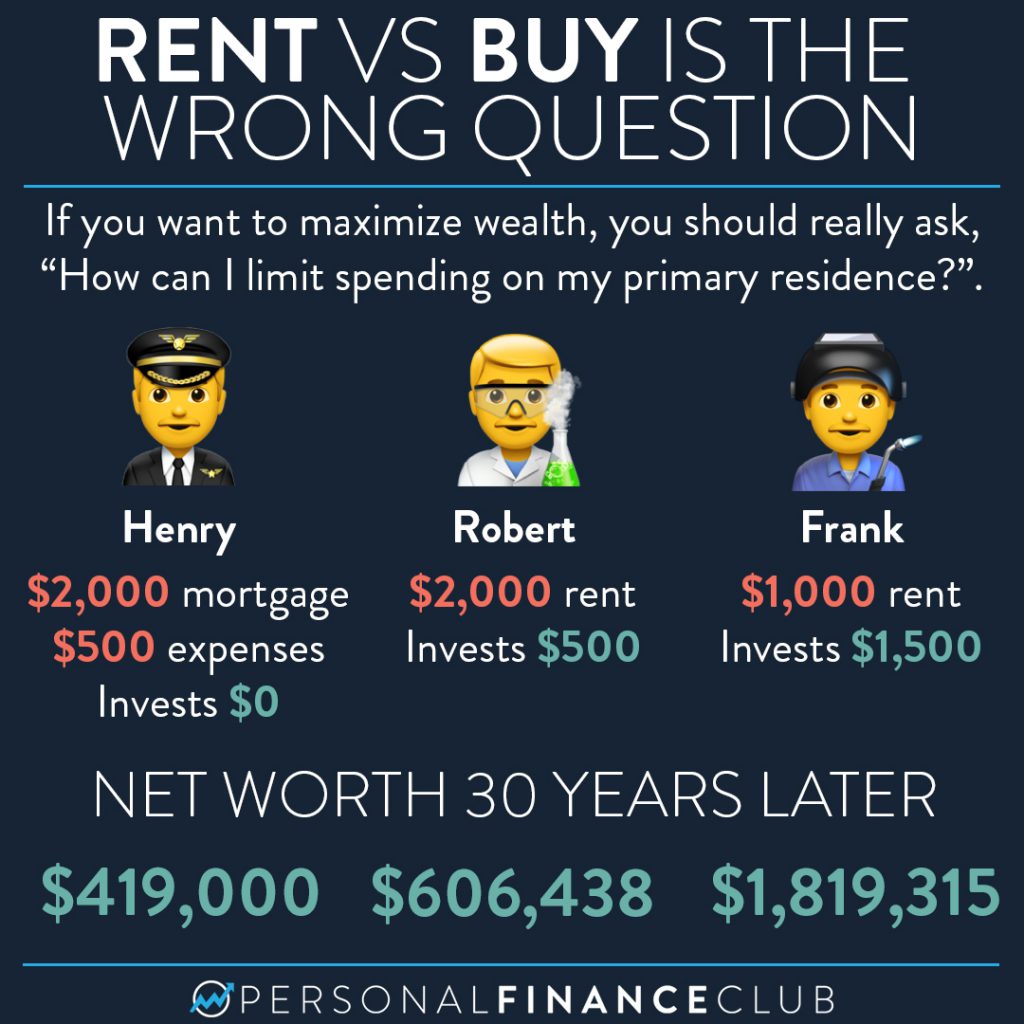

This is the point where homeowners and realtors get out their pitchforks and want to skewer me for suggesting renting is better than buying. Renting costs money too! Taxes, insurance, maintenance, utilities, etc are all built into the rent, plus profit for the landlord! That’s all true. But that’s where the “rent vs buy” question fails us. Just because renting is a bad investment doesn’t mean that buying is good. They’re both an expense. Having a roof over your head is going to cost you money no matter how you do it. There’s a third option in the rent vs buy debate: Spend less.

The real path to maximizing wealth is minimizing the expense of your residence and focusing your investing dollars elsewhere. So many fall into the trap of renting modestly than buying extravagantly (“it’s an investment after all!”). That’s the real danger of buying. Whether you rent or buy, do it more modestly and put those extra dollars into great investments like buying and holding index funds or investment real estate. (The math on real estate changes dramatically when you are getting an income stream on top of the 3.8% historical appreciation).

So Why Did I Buy?

If buying is such a bad investment, why did I just do it? Well, for reasons despite the financial costs. I wanted to move closer to the beach. Have a spare bedroom for guests. The ability to remodel and make it my own. And, frankly, because I could afford it. I never got in way over my head paying an expensive mortgage when I had a small income.

I did this all with my eyes wide open that it would be very likely to hurt my net worth growth going forward. I bought relatively conservatively. About 20% of my net worth is now tied up in my primary residence not generating income and appreciating slowly. The other 80% is out in the world working for me, paying dividends and providing rental income.

As always, reminding you to build wealth by following the two PFC rules: 1.) Live below your means and 2.) Invest early and often.

– Jeremy