At its core, insurance is a pretty simple concept. You make a deal with a company. “I’ll pay you a little bit of money every month and in exchange if this rare but very expensive thing happens, you pay me some or all of the big cost”. That’s really all it is. Spending a little bit of money to mitigate the risk of something very expensive happening. For example, houses don’t usually burn down, but if they do it’s financially catastrophic. So homeowners generally pay a little bit of money per month so if their house DOES burn down the insurance company pays the bill.

This works for insurance companies because they always make sure to collect more money than they pay out. They’re good at figuring out how often something happens, then how much they have to charge to cover it when it does leaving profit for themselves.

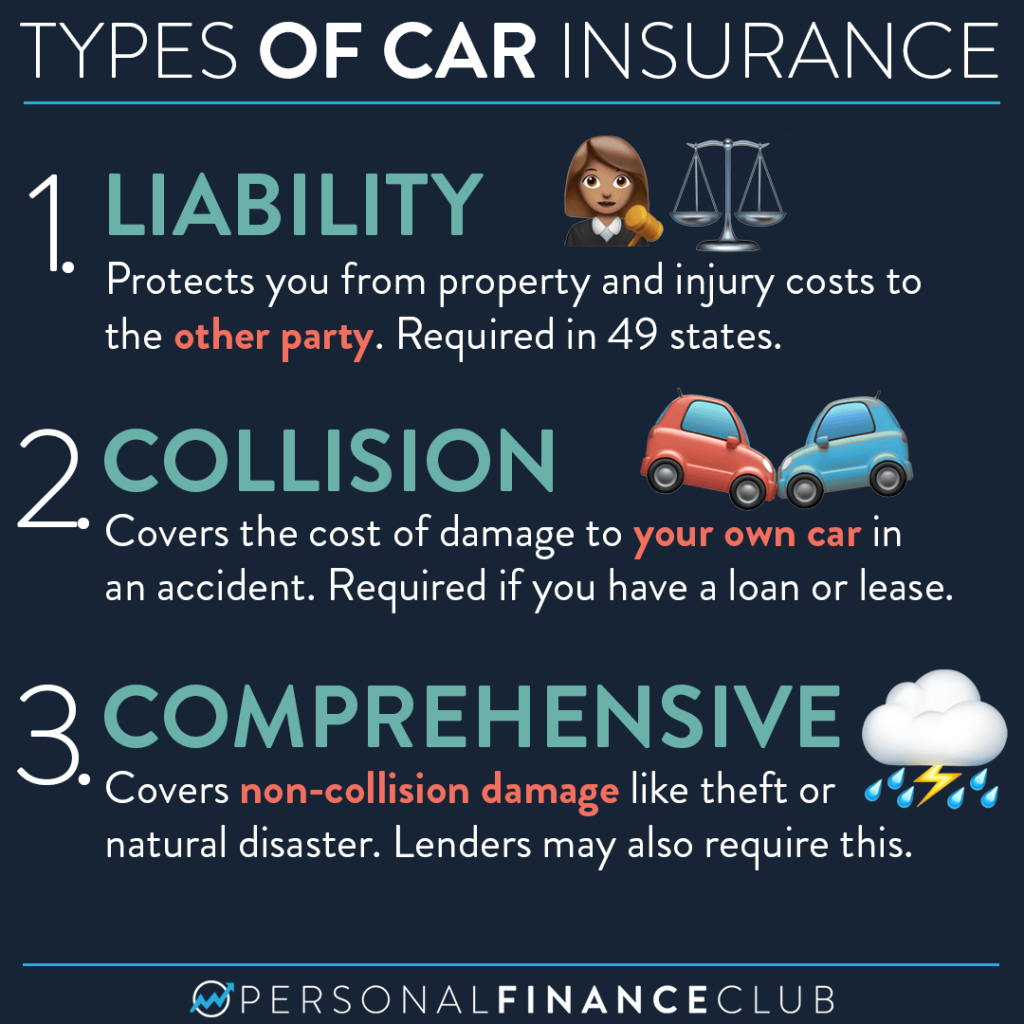

Car insurance is pretty much the same. But it can get complicated because because there’s not just one “deal” you can make with the insurance company. They break it up and sell it individually so you can decide WHICH bad things you want to financially protect yourself from.

For example, if you own your car free and clear, no one requires you to carry collision insurance. If you get in a crash and your car is destroyed you can just eat the cost and buy a new car. I never carried collision insurance on my last car. That’s because my car was very cheap. The resale value was about $1,500. That was an amount of risk I was willing to accept, so there was no reason to pay a monthly bill to avoid it. I bought my current car for about $32,000 and I did choose to pay for collision because I didn’t want to foot a $32,000 bill if I crashed it the day I drove off the lot. But now it’s almost 5 years old and worth less than half of that 😭 so I’m probably going to drop collision soon as I can “self insure” the replacement cost.

As always, reminding you to build wealth by following the two PFC rules: 1.) Live below your means and 2.) Invest early and often.

-Jeremy

via Instagram

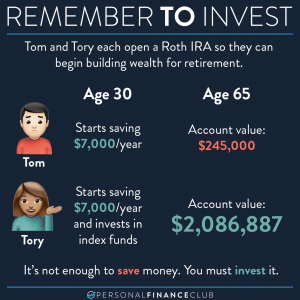

Why saving money is not enough? – you MUST invest it

Forgetting to invest in our example, resulted in an almost $2 MILLION dollar mistake. Don’t let this be you. Stop what you’re doing and make